How to change homeowners insurance? The short answer is that changing your homeowners insurance is a straightforward process that involves securing a new policy, ensuring there is no lapse in coverage, and notifying your mortgage lender to update your escrow payments. You do not need to wait for your annual renewal date to make a move. In the current 2026 “hard market,” US homeowners are facing unprecedented rate hikes, with national average premiums rising 12.4% year-over-year according to recent S&P Global Market Intelligence data. This volatility makes the ability to switch carriers your most important financial defense.

I’m the Insurance Cop, and I’ve built this guide to serve as your tactical “enforcement manual.” Most homeowners feel a misplaced sense of loyalty to their insurance company, but the industry often rewards that loyalty with a “loyalty penalty”, creeping rates that target customers who don’t shop around. This guide is designed to serve as your roadmap for managing a switch from start to finish. We will resolve everything from how to change homeowners insurance with escrow to the legal nuances of mid-term refunds, ensuring your most valuable asset remains protected by the best math available.

Mastering your policy math means knowing exactly which events trigger your coverage. For example, knowing does homeowners insurance cover lightning strikes and how it impacts your personal property limits is a foundational part of being a prepared homeowner.

Can you change homeowners insurance at any time?

Yes, you have the legal right to cancel your homeowners insurance and switch to a new provider at any point during your policy term. You are not “locked in” until your annual renewal date, nor do you need a “qualifying life event” (like a move or a marriage) to change companies. In all 50 US states, insurance is a voluntary contract that can be terminated by the policyholder at will.

If you find a better rate today, you can technically fire your current carrier tomorrow. However, to execute this move like a professional, you should keep these “Insurance Cop” rules in mind:

- The Pro-Rata Right: When you cancel mid-term, insurers are required to refund your “unearned premium”, the money you paid in advance for the months of coverage you didn’t use.

- The Binding Rule: The Insurance Cop’s #1 rule is to never cancel your old policy until the new one is bound and active. A 24-hour gap in coverage can disqualify you from “continuous coverage” discounts and leave you vulnerable.

- The 12:01 AM Handover: Most policies start and end at 12:01 AM. Ensure your new policy starts on the same day your old one ends to ensure a seamless transition.

“Consumers are often surprised to learn they aren’t stuck. If your insurer isn’t competitive, the best time to switch is the moment you find a better option. You own the contract; the carrier doesn’t own you.” – Mark Friedlander, Director of Corporate Communications at the Insurance Information Institute.

Understanding the legal timeline of your policy is the first step toward savings. For a detailed breakdown of your rights and the “Short-Rate” traps to avoid, read our dedicated guide on ‘Can You Change Homeowners Insurance at any time?‘.

Does homeowners insurance automatically renew?

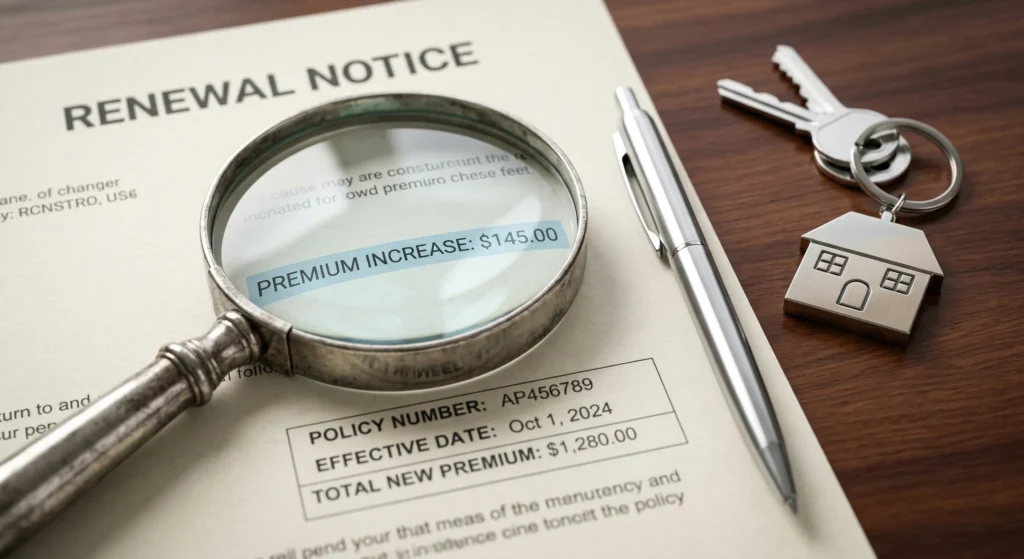

Yes, most homeowners insurance policies are written with a “Continuous Renewal” clause, meaning they will automatically renew each year unless you or the carrier provides written notice of cancellation. This is designed to prevent homeowners from accidentally becoming uninsured. However, while automatic renewal provides convenience, it is also the mechanism carriers use to implement “silent rate hikes.”

The Insurance Cop red-flags automatic renewals because they often lead to “set it and forget it” behavior. At least 30 to 60 days before your policy expires, your carrier will send a renewal notice. This document contains the new premium for the upcoming year. If your insurance is paid through escrow, your lender will receive this bill and pay it automatically. If you don’t scrutinize this notice, you could be opting into a 15% rate hike without realizing it.

Renewal vs. Non-Renewal:

- Automatic Renewal: The carrier wants to keep you but may change the price.

- Non-Renewal: The carrier has decided to stop insuring your property (common in 2026 in high-risk zones like Florida or California). They must legally notify you 30-60 days in advance.

Most homeowners forget that their policy is likely on autopilot. I have broken down the specific mechanics of how does homeowners insurance automatically renew and how to stop it in my tactical cycle guide.

How to Change Homeowners Insurance Step-by-Step Guide

To change your homeowners insurance correctly, you must follow a specific sequence: audit your current coverage, secure and bind a new policy with an overlapping start date, and only then issue a formal cancellation notice to your previous carrier. Skipping a step or miscalculating the timing can lead to a “coverage gap,” which not only leaves your home vulnerable but can also trigger a “force-placed” policy from your mortgage lender, often costing three times the price of a standard plan.

I have broken down the 2026 GTHI “Enforcement Protocol” into five non-negotiable steps to ensure your transition is seamless.

Step 1: The Coverage Audit

Before you look for a cheaper price, you must ensure you aren’t trading protection for a lower premium. Look at your current Declarations Page. Is your “Coverage A” (Dwelling) based on 2026 replacement costs? Use the Replacement Cost Calculator to verify this. As Amy Bach, Executive Director of United Policyholders, warns: “Matching a low price is easy for a carrier; matching the actual cost to rebuild your life after a total loss is where the fine print matters.” Ensure your new quote includes “Replacement Cost Value” (RCV) for both the structure and your personal property.

Step 2: Shop and Compare

When shopping, don’t just get one quote. Get three. Look for carriers with an AM Best rating of ‘A’ or higher. When you find the right provider, answer their underwriting questions honestly. In 2026, many carriers are using high-resolution satellite imagery to inspect roofs before they even offer a quote. If your roof is over 15 years old, be prepared for a “limited roof payment” endorsement or a requirement for a physical inspection.

Step 3: Bind the New Policy First

The Insurance Cop’s Golden Rule: Never cancel Policy A until Policy B is “Bound.” In insurance terms, “binding” means the carrier has accepted your risk and the policy is legally active. You will likely need to pay the first month’s premium (or the full year if not in escrow) to bind the policy. This ensures that you have a “Policy Binder” to show your mortgage company as proof of continuous coverage.

Step 4: Synchronize the 12:01 AM Handover

In the United States, almost all homeowners policies begin and end at 12:01 AM. To avoid a lapse, set your new policy to start on the exact same date that you intend to cancel your old one.

- Example: If you want your old coverage to end on April 1st, set your new coverage to begin at 12:01 AM on April 1st. This creates a “seamless handoff” that satisfies lender requirements and keeps your “continuous coverage” discount intact.

Step 5: Formal Cancellation and Mortgage Notification

Once you have your new policy number and effective date, contact your old insurance company to sign a formal “Cancellation Request.” A phone call is usually not enough; most carriers require an e-signature or a written letter. Finally, if your insurance is paid through your mortgage, you must send the new policy’s “Declarations Page” to your lender’s insurance department. This prevents them from double-billing your escrow account.

How to change homeowners insurance with an escrow account?

To change homeowners insurance with an escrow account, you must secure a new policy, provide the “Policy Binder” to your mortgage servicer, and ensure the new premium is paid out of your escrow reserves. If your mortgage lender manages your insurance payments through an escrow account, they are technically the ones who “cut the check” to the insurance company. However, as the homeowner, you remain the owner of the contract and have the full right to change providers whenever you find better value.

The most common point of confusion in the homeowners insurance claim process regarding escrow is the “refund loop.” When you switch carriers mid-term, your old insurance company will send a refund check for the unused months directly to you, not to your bank. Conversely, your new insurance company will send the bill for the full year directly to your bank.

The Insurance Cop’s Escrow Protocol

- The “Double Payment” Warning: Because it can take 30 days for a lender to process a new bill, your escrow account might temporarily look like it is in a “shortage.”

- Deposit the Refund: Since you received the refund check from the old carrier, you should ideally send that money into your escrow account to cover the new bill your lender just paid.

- Check the Analysis: Under the Real Estate Settlement Procedures Act (RESPA), your lender must perform an annual escrow analysis. Switching mid-term can trigger a new analysis, which might slightly increase or decrease your monthly mortgage payment.

Managing a carrier switch while a lender holds your funds in a third-party account requires specific documentation. If your premiums are paid through your mortgage, you must follow our detailed tactical breakdown on how to change homeowners insurance with escrow to ensure your bank receives the correct bill and you receive your refund check safely.

Do you get a refund if you cancel homeowners insurance?

Yes, you are legally entitled to a refund of the “unearned premium” when you cancel your homeowners insurance policy before its expiration date. Since most homeowners pay for their insurance a full year in advance (either via escrow or a lump sum), the insurance company is holding money for months of protection they haven’t actually provided yet. If you cancel on day 100 of a 365-day policy, the carrier is holding 265 days’ worth of your cash.

However, the amount of your refund depends on the “Cancellation Clause” in your policy’s fine print. The Insurance Cop red-flags carriers that use “Short-Rate” math to penalize departing customers.

Refund Math 101

- Pro-Rata Refund (The Fair Way): The carrier returns 100% of the unused premium. If you paid $1,200 for a year and cancel with 6 months left, you get $600 back.

- Short-Rate Refund (The Penalty Way): The carrier keeps an administrative fee (often 10% of the unearned portion). Using the example above, you might only get $540 back.

- Timeline: According to the Insurance Information Institute (III), you should expect your refund check within two to four weeks after the cancellation is processed.

Pro-Tip: Always demand a “Pro-Rata” cancellation. If the agent tells you there is a fee, ask them to point out the specific “Short-Rate Table” in your policy. If it isn’t there, they can’t charge it.

Securing your refund is what makes a policy switch financially profitable. To help you calculate your daily rate and spot hidden administrative fees, I’ve put together a full breakdown on do you get a refund if you cancel homeowners insurance in our 2026 technical guide.

When to cancel homeowners insurance when selling house?

You should cancel your homeowners insurance on the day after the official closing of the sale, ensuring that the deed has been recorded and you are no longer the legal owner of the property. One of the most dangerous mistakes a seller can make is canceling their policy the moment they sign the contract or move out of the house. Until the “Closing Disclosure” is signed and the money has changed hands, you are still liable for everything that happens on that property.

The Insurance Cop’s “Sale Safety” Checklist

- The Gap Trap: If a fire occurs two hours before closing and you have already canceled your policy, you are personally responsible for the loss, and the sale will likely collapse.

- Post-Sale Liability: Even after you move out, if a pipe bursts before the buyer takes possession, your policy is your only shield.

- Proof of Sale: To trigger your refund after selling, your insurer will usually require a copy of the “Settlement Statement” (HUD-1) showing the date the ownership was transferred.

If you are moving out because you just closed on a sale, the timing becomes even more critical than a standard carrier switch. You don’t want to leave your equity exposed during those final few hours of the handover. I have put together a specific tactical roadmap on when to cancel homeowners insurance when selling a house that explains the 24-hour buffer you need to stay safe until the deed is officially recorded.

How to find my homeowners insurance?

The fastest way to find your homeowners insurance information is to contact your mortgage lender, search your email for “Declarations Page,” or review your recent bank and credit card statements for premium payments. Because homeowners insurance is a requirement for almost all US mortgages, your bank is required to keep an active record of your policy number, carrier, and coverage limits on file.

If you don’t have a mortgage and have lost your physical policy binder, the Insurance Cop recommends these three tactical recovery steps:

- The Mortgage Hub: Call your lender’s insurance or escrow department. They can provide your policy number and the carrier’s contact information in minutes.

- The Digital Paper Trail: Search your email inbox for keywords like “Renewal,” “Binder,” “Policy,” or “Insurance.” Most carriers in 2026 default to electronic delivery for the “Dec Page.”

- Check the C.L.U.E. Report: As a last resort, you can request a copy of your Comprehensive Loss Underwriting Exchange (C.L.U.E.) report from LexisNexis. This report lists your insurance claim history and the carriers you’ve been insured with over the last seven years.

I spend a lot of time policing the fastest ways to recover data when a policy binder goes missing. If you’re stuck at the first step of a switch, I’ve put together a tactical recovery roadmap on how to find my homeowners insurance that shows you how to leverage your lender and email archives in minutes.

How to find out homeowners insurance by address?

You cannot legally look up a private individual’s insurance policy details simply by searching an address due to privacy laws; however, you can verify if a property is insured by checking public county records, reviewing an insurance binder during a home purchase, or requesting a C.L.U.E. report for a property you own. Insurance policies are private contracts between a homeowner and a carrier, and this information is not part of the public domain in the same way property tax records are.

However, if you are a buyer or an heir and need to know how to find out homeowners insurance by address, you have specific legal pathways:

- During the Escrow Process: If you are buying a home, the seller’s agent will provide an “Insurance Binder” or proof of existing coverage to ensure the property is protected until the title transfers.

- Public Tax Records: Some county tax assessors in states like Texas or Florida track whether a property is “Insured” if the taxes and insurance are paid through a public escrow program, though they will not list specific policy details.

- Title Company Records: If you have recently closed on a home, the title company or the closing attorney will have the insurance information used during the settlement in their records.

According to the Consumer Financial Protection Bureau (CFPB), lenders use address-based tracking to ensure every mortgaged property has a “Loss Payee” clause. If you are an owner trying to remember which carrier you chose, checking your closing documents is the most reliable “address-based” search method.

How long to keep homeowner insurance policies?

You should keep your homeowners insurance policy documents for at least seven years, even after you have switched carriers or sold the property. While it may seem unnecessary to keep paperwork for an expired contract, old policies serve as your only financial protection against “latent damage” claims, issues like slow-leaking pipes or structural cracks that may have originated years ago while an old policy was still active.

The Insurance Cop’s “7-Year Rule” Breakdown

- Liability Protection: If someone sues you in 2026 for an injury that occurred on your property in 2024, you need the policy that was active at the time of the injury to cover your legal defense.

- Tax Audits: If you have claimed a home office deduction, the IRS may require proof of insurance premiums paid during the audit window.

- The Digital Archive: I recommend scanning your “Declarations Pages” and saving them to a secure, encrypted cloud drive. This ensures that even if a fire destroys your physical records, your proof of coverage remains intact.

One question I get asked constantly is what happens to your old paperwork once the switch is done. I’ve policed the legal timelines and found that knowing how long to keep homeowner insurance policies is the only way to protect yourself from latent claims that pop up years after you’ve left a carrier.

How to sell homeowners insurance

To sell homeowners insurance professionally in the United States, an individual must obtain a Property and Casualty (P&C) insurance license from their state’s regulatory body and choose between operating as a “Captive” agent for one company or an “Independent” agent representing multiple carriers. Understanding the industry side of the desk helps you, the homeowner, recognize the incentives driving your agent. When you are looking at how to change homeowners insurance, you are essentially navigating the sales models of these professionals.

At Guide to Home Insurance, we advocate for the independent agency model. Independent agents have the ability to “shop” your policy across 10 to 20 different carriers, whereas captive agents (like those at State Farm or Allstate) are restricted to their company’s specific rates and appetites. In the 2026 market, carriers are frequently “pausing” new business in certain zip codes; an independent agent is often the only way to find a carrier still willing to write a policy in a high-risk zone.

According to the Independent Insurance Agents & Brokers of America (IIABA), independent agents now control over 35% of the homeowners market because they provide the mobility consumers demand. If you are learning the industry to switch careers or just to better understand your own policy, remember that the most successful agents are those who act as consultants, not just order-takers.

If the process of auditing your policy has sparked a genuine interest in the industry, you might be curious about the other side of the desk. I’ve policed the professional landscape and created a master briefing on how to sell homeowners insurance that covers everything from state licensing to the choice between independent and captive business models.

The GTHI 2026 Switching Scorecard

Before you finalize a policy change, the Insurance Cop requires you to run your new quote through our proprietary Switching Scorecard. A lower premium is a “green flag,” but it doesn’t always mean a better deal. Use this 5-point matrix to determine if your $200 or $500 savings is worth the transition.

| Category | High Value (Score: 5) | Red Flag (Score: 1) |

| Financial Strength | AM Best Rating of A+ or higher. | AM Best Rating below B or Unrated. |

| Deductible Delta | Standard $1,000 or $2,500 All-Peril. | Hidden 2% or 5% Wind/Hail Deductible. |

| Valuation Type | Guaranteed Replacement Cost (RCV). | Actual Cash Value (ACV) on the roof. |

| Claims Reputation | High JD Power Customer Satisfaction score. | Excessive “Bad Faith” complaints at state DOI. |

| Endorsement Depth | Includes Sewer Backup and Service Line. | Minimalist policy with “Standard” exclusions. |

How to use the Scorecard

If your new policy scores below a 15 out of 25, you aren’t “saving” money, you are increasing your financial risk. Often, the lowest-priced carriers in 2026 are those that have stripped away the “Ordinance or Law” or “Water Backup” riders to make the headline premium look attractive.

“Price is what you pay; value is what you get when your house is gone. If the switch involves moving from a 1% deductible to a 5% deductible, you aren’t saving money; you are just moving the debt to your future self.” – Insurance Cop’s Enforcement Rule #12.

Answers to Common Switching Questions

Below are the technical, long-form responses to the most frequent homeowners insurance questions our researchers receive regarding the policy change process.

No, the act of switching insurance companies does not directly impact your FICO credit score. Unlike a loan application, insurance “hard hits” are rare. However, most carriers use a Credit-Based Insurance Score to determine your rate. While this is a “soft pull” that doesn’t hurt your credit, the insurer is looking at your history of managing debt to predict your likelihood of filing a claim. According to FICO, homeowners with higher credit-based insurance scores can pay up to 40% less for the same policy.

No, your mortgage company cannot legally prevent you from changing your insurance provider, provided the new policy meets their minimum coverage requirements. Under federal law, the lender’s only interest is ensuring their collateral (your home) is protected. If you provide them with a valid “Policy Binder” showing “Coverage A” matches your loan balance and that they are listed as the “Mortgagee/Loss Payee,” they are required by RESPA regulations to accept the change and update your escrow account.

In 2026, the answer is increasingly yes. Due to the “Hard Market,” carriers are highly selective. They often use high-resolution drone or satellite imagery to inspect your roof’s condition immediately. If they see moss, curling shingles, or overhanging trees, they may issue a “Notice of Cancellation” effective 30 days after the policy starts unless the repairs are made. Always perform a self-inspection of your property before switching to avoid an immediate “red-flag” from the new carrier.

This is a critical math question. A Pro-Rata refund is a simple division: if you used 25% of the year, you get 75% of your money back. A Short-Rate refund allows the insurance company to keep a penalty, often 10%, of the remaining premium as a “cancellation fee.” While most states discourage short-rate math for homeowners, some carriers still hide it in the fine print. Always ask: “Are you charging me a short-rate penalty for this mid-term move?”

Not necessarily. While “Bundling” is the #1 marketing tool used by carriers, the Insurance Cop has found that in high-risk states, the bundle is sometimes a trap. In 2026, we are seeing cases where an independent auto policy combined with a specialized home policy from a different carrier results in $400+ annual savings compared to a bundle. Never assume the bundle is the best math; always request “standalone” quotes to compare.

Enforcing Your Right to a Better Policy

The primary takeaway is that learning how to change homeowners insurance is the most effective way to regain control over your household’s financial protection. In an era of shifting climate risks and rising labor costs, a policy you bought three years ago is likely outdated. By following the steps outlined in this guide, auditing your coverage, synchronizing your effective dates, and managing your escrow transition, you ensure that your home remains shielded by a contract that reflects the realities of 2026.

As the Insurance Cop, my final piece of advice is this: Never let an insurance company mistake your loyalty for a lack of options. The industry operates on data and risk; you must operate on the same level of scrutiny. Switching providers isn’t just about saving $20 a month; it’s about ensuring that if the “worst-case scenario” happens tomorrow, your policy is built to rebuild your life, not just settle a debt.

The Insurance Cop’s Final “Safe-Switch” Checklist

- Verify the Carrier: Check the AM Best rating of any new company before signing.

- Check the Deductible: Ensure a lower premium didn’t come from a hidden 2% or 5% wind/hail deductible.

- Confirm the Payout: Demand “Replacement Cost Value” (RCV) for your personal belongings.

- Notify the Lender: Don’t let your mortgage company double-bill your escrow account because you forgot to send the new binder.

Your home is your most valuable asset. Treat the contract that protects it with the respect and vigilance it deserves.

[NEXT STEP] Don’t Switch to the Wrong Coverage Limits

Now that you’ve mastered how to change homeowners insurance, make sure your new policy actually covers your home’s 2026 value. Many carriers suggest limits based on outdated algorithms that don’t account for the current 12.4% spike in construction labor costs.

Before you sign your new contract, use our Free Replacement Cost Calculator Toolkit to “police” your new quote. Get precise, zip-code-specific math for your:

- Total Rebuild Value 🏠

- Roof Replacement 🧱

- Window & System Upgrades 🪟