When disaster strikes your home, your insurance policy is meant to be your financial lifeline. However, the path from initial damage to a final settlement check is often filled with complex requirements and strict deadlines. Successfully managing property insurance claims requires more than just paying your premiums; it requires a proactive approach to documentation and a deep understanding of how the property damage insurance claims process actually works.

Many policyholders feel overwhelmed by the technicalities of homeowners insurance claims, often leading to avoidable delays or undervalued payouts. According to the Insurance Information Institute (III), the actions you take in the first 24 to 48 hours after a loss are the most critical. By following a structured homeowners insurance claim process, you can ensure that you meet all contractual obligations while protecting your right to a fair appraisal.

In this guide, we break down everything you need to know about filing and managing property damage insurance claims, from emergency mitigation steps to final repairs. Our goal is to transform a confusing situation into a manageable set of actions, giving you the confidence to advocate for your home’s restoration.

Understanding the Property Damage Insurance Claim

A property damage insurance claim is a formal request submitted to your insurance provider, asking for compensation to repair or replace assets that have been damaged. In simple terms, your insurance policy is a contract where the insurer agrees to indemnify you against specific losses in exchange for your premiums. When you file a claim, you are officially asking them to fulfill that agreement.

However, just because damage has occurred doesn’t always mean you should immediately file a property damage insurance claims process. As a general rule of thumb, you should weigh the estimated cost of repairs against your policy deductible. If your roof repair costs $800 and your deductible is $1,000, paying out-of-pocket is often the wiser financial choice. This is because insurance carriers utilize a database to track your claims history; frequently filing small homeowners insurance claims can brand you as a high-risk policyholder, resulting in premium increases or non-renewal upon your next policy term.

According to the National Association of Insurance Commissioners (NAIC), knowing when to file is just as important as knowing how to file. Generally, you should reserve property insurance claims for losses that exceed your deductible by a significant margin, such as severe weather damage, structural failures, or major fire incidents, to protect your long-term financial standing.

For a deeper understanding of how your claims history affects your policy, you can review the industry standards on loss history reports provided by LexisNexis regarding the CLUE report.

Immediate Steps: What to Do Right After Damage Occurs

The moments immediately following a loss are often chaotic, but they are also the most critical for the success of your property damage insurance claim. Before you even pick up the phone to call your agent, your first priority must be safety and the prevention of “secondary damage.” In the insurance world, this is known as your duty to mitigate.

- Prioritize Safety: If the damage is structural, involves standing water near electrical outlets, or if you smell gas, evacuate immediately. Do not re-enter the home until local authorities or licensed professionals have deemed it safe.

- Prevent Further Damage: Most homeowners insurance claims include a clause requiring you to take “reasonable steps” to protect the property from further harm. This might include:

- Tarping a damaged roof to prevent rain from entering.

- Boarding up broken windows or doors to deter theft or vandalism.

- Shutting off the main water valve to stop a leak.

- Document Before You Repair: While you should make temporary repairs to stop further loss, do not begin permanent restoration or throw away damaged items until you have captured extensive evidence. Use your smartphone to take high-resolution photos and videos from multiple angles.

- Keep Every Receipt: Any money you spend on emergency mitigation, such as buying plywood, tarps, or hiring a water extraction team, is typically reimbursable. According to the Federal Emergency Management Agency (FEMA), keeping an organized file of these “out-of-pocket” mitigation expenses is vital for your final settlement.

- Start a Communication Log: From the very first minute, document who you speak with, the date and time of the call, and a summary of what was discussed. This log becomes an invaluable piece of evidence if the homeowners insurance claim process faces delays or disputes later on.

By taking these proactive measures, you demonstrate to the insurer that you are a responsible policyholder, which can significantly smoothen the property damage insurance claims process as it moves into the evaluation phase.

The Homeowners Insurance Claim Process: Step-by-Step

The homeowners insurance claim process can take anywhere from a few days to several months, depending on the severity of the damage and the responsiveness of your carrier. By understanding the typical lifecycle of property damage insurance claims, you can maintain control and ensure no details are overlooked during the transition from “loss” to “repair.”

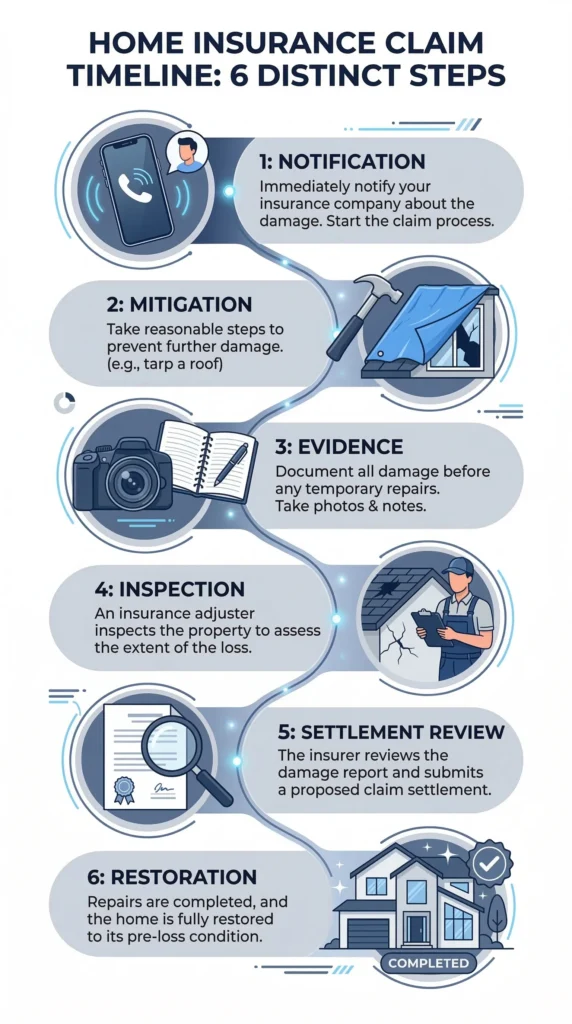

Step 1: Immediate Notification

As soon as you have stabilized the property and ensured everyone’s safety, notify your insurance company or agent. Most providers offer a 24/7 claims hotline or a mobile app to initiate the property damage insurance claims process. Be prepared to provide your policy number and the date of the loss. At this stage, ask for your claim number and the name of the assigned adjuster so you can track all future correspondence.

Step 2: Emergency Mitigation

In almost all property insurance claims, the policyholder has a “duty to mitigate.” This means you must take reasonable steps to prevent further damage. Whether it’s tarping a roof, boarding up windows, or drying out water, these temporary repairs are essential. Keep all receipts for materials and labor, as these are typically reimbursable under your coverage.

Step 3: Comprehensive Evidence Collection

Before the adjuster arrives, you need to be your own investigator. Create a detailed inventory of all damaged personal property and take high-resolution photos and videos of the structural damage. According to the National Association of Insurance Commissioners (NAIC), having a thorough “Proof of Loss” document ready can significantly speed up the evaluation phase of homeowners insurance claims.

Step 4: The Adjuster’s Inspection

The insurance company will send a claims adjuster to inspect the damage and verify the cause of loss. During this walkthrough, point out every area of concern you documented in Step 3. Do not assume the adjuster will see everything; being present and proactive ensures that “hidden” damage is noted early in the property damage insurance claims process.

Step 5: Reviewing the Settlement Offer

Once the inspection is complete, the insurer will provide a settlement estimate. This document outlines what they are willing to pay based on your policy’s limits and valuation (ACV vs. RCV). It is vital to review this carefully. Organizations like United Policyholders recommend comparing this offer against quotes from independent contractors to ensure the payout is sufficient to cover the actual cost of repairs.

Step 6: Restoration and Supplemental Claims

After you accept the settlement and repairs begin, your contractor may discover additional damage that wasn’t visible during the initial inspection. In these cases, you can file a “supplemental claim” to cover the extra costs. Once the repairs are finished and all supplemental payments are issued, the homeowners insurance claim process is officially concluded.

Essential Documentation for Your Claim

When you file a property damage insurance claim, the burden of proof lies with you, the policyholder. You must be able to demonstrate exactly what was damaged, the condition it was in prior to the loss, and the cost to restore or replace it. Proper documentation turns your word into a verifiable fact, making the property damage insurance claims process much smoother for both you and the adjuster.

To ensure your homeowners insurance claims are processed accurately, organize the following documents into a dedicated “Claims Folder” (either physical or digital):

Comprehensive Visual Evidence

Before cleaning up or removing debris, take high-resolution photos and videos of the damage from multiple angles. Capture wide shots to show the scope of the event and close-up shots of specific structural damage or destroyed items.

The “Proof of Loss” Inventory

Create a detailed list of every piece of personal property that was damaged or stolen. Include the description, age, approximate purchase price, and a link to a replacement item if possible. According to Consumer Reports, having a pre-existing home inventory can save weeks of stress during this phase.

Receipts for Emergency Repairs

As mentioned in Section 3, any money spent on tarping, boarding up, or water extraction should be documented with original receipts. These are almost always reimbursable as part of your property insurance claims.

Living Expense Records (ALE)

If the damage is severe enough that you cannot live in your home, keep every receipt for hotels, restaurant meals, and even additional mileage driven. These fall under “Additional Living Expenses” (Coverage D).

The Communication Log

Maintain a running record of every interaction with your insurance company. Note the date, time, the name of the person you spoke with, and a summary of the conversation. If there is a dispute later in the property damage insurance claims process, this log serves as a vital chronological record of the insurer’s promises and timelines.

Working with the Insurance Adjuster

Once you have notified your provider, they will assign an adjuster to handle your property damage insurance claim. It is important to remember that while the adjuster is typically professional and helpful, they are employees or contractors of the insurance company. Their primary goal is to evaluate the loss based on the specific language of your policy.

To ensure your homeowners insurance claims are evaluated fairly, follow these best practices when working with your assigned adjuster:

- Be Present During the Inspection: Never let an adjuster inspect your property alone. You know your home better than anyone else. By being present, you can point out subtle damage that an adjuster might overlook, such as small cracks in the foundation or water stains inside a closet.

- Have Your Documentation Ready: When the adjuster arrives, provide them with a copy of the “Proof of Loss” inventory and the photos you took immediately after the damage occurred (as discussed in Section 5). This proactive approach sets a professional tone for the property damage insurance claims process.

- Discuss the “Cause of Loss”: Under many property insurance claims, the cause of the damage determines if it is covered. Be honest and clear about what happened. If the damage was caused by a “Named Peril” like wind or fire, ensure the adjuster’s report reflects that accurately.

- Don’t Feel Pressured to Sign Immediately: Adjusters sometimes offer an “on-the-spot” settlement check. While this can be tempting, it is often better to wait until you have a full contractor’s estimate. Once you cash a final settlement check, it can be much harder to request more money later.

- Understand the Different Types of Adjusters: You may encounter a Staff Adjuster (employed by the carrier) or an Independent Adjuster (hired by the carrier during busy times). If you feel your claim is being unfairly handled, you have the right to hire a Public Adjuster, who works specifically for you, though they typically charge a fee based on the settlement.

According to the California Department of Insurance, maintaining a professional and cooperative relationship with your adjuster, while remaining firm on the facts of your damage, is the most effective way to navigate the homeowners insurance claim process successfully.

The final phase of the homeowners insurance claim process involves the settlement offer and the physical restoration of your property. Understanding how your payout is calculated and how the funds are released is crucial for managing your repair budget effectively. In many property insurance claims, the money doesn’t arrive in one single check, and there are often specific rules on how that money can be spent.

- The Two-Check System (RCV vs. ACV): If you have Replacement Cost Value (RCV) coverage, it is common for the insurer to pay property damage insurance claims in two installments. The first check is for the Actual Cash Value (ACV), the value of the damage minus depreciation. The second check, often called “recoverable depreciation,” is issued only after you provide proof that the repairs are complete.

- The Role of Your Mortgage Lender: If you have a mortgage, your lender has a financial interest in the property and is usually listed as a “Loss Payee.” This means the check for homeowners insurance claims will likely be made out to both you and the mortgage company. You will need to contact your lender to have them “endorse” the check or place it in an escrow account to pay contractors as work progresses. According to the Consumer Financial Protection Bureau (CFPB), this ensures the home is actually repaired to its original value, protecting the lender’s collateral.

- Choosing the Right Contractor: While your insurance company may suggest a “preferred vendor,” you generally have the right to hire any licensed contractor you choose. Ensure your contractor reviews the adjuster’s estimate before work begins. If their costs are higher, they can work with the insurer to request a “supplement” before the property damage insurance claims process is finalized.

- Holdbacks and Deductibles: Remember that your insurance company will subtract your deductible from the final settlement. For example, if your total repair cost is $10,000 and your deductible is $1,000, the total payout for your property insurance claims will be $9,000. You are responsible for paying the $1,000 difference directly to your contractor.

By understanding these financial nuances, you can avoid surprises and ensure that the homeowners insurance claim process concludes with your home fully restored without unexpected out-of-pocket burdens.

Common Pitfalls in Homeowners Insurance Claims

Even when you follow the homeowners insurance claim process carefully, small mistakes can lead to significant setbacks, undervalued payouts, or even denied claims. The insurance contract is a legal document with strict requirements, and failing to meet them can jeopardize your recovery.

To ensure your property insurance claims stay on track, avoid these common pitfalls that many policyholders encounter during the property damage insurance claims process:

- Delaying the Initial Filing: Most insurance policies have a “statute of limitations” or a specific window of time (often 30 to 60 days) in which you must report a loss. Waiting too long to start homeowners insurance claims can give the insurer grounds to deny the claim, especially if the delay made it harder to investigate the cause of damage.

- Discarding Damaged Items Too Soon: It is a natural instinct to want to clean up after a disaster, but throwing away damaged furniture, appliances, or debris before the adjuster inspects them is a major mistake. If the evidence is gone, the insurer may refuse to pay for it. Always wait for the “OK” from your adjuster before hauling debris to the landfill.

- Failing to Mitigate Damage: As discussed in Section 3, you have a legal duty to prevent further loss. If a small roof leak turns into a massive mold problem because you didn’t put up a tarp, the insurance company may only pay for the roof repair and deny the mold remediation costs.

- Inaccurate or Incomplete Documentation: Providing vague descriptions or “guessing” the value of items can lead to delays. According to the National Association of Public Insurance Adjusters (NAPIA), precision is key. A property damage insurance claim backed by receipts, model numbers, and clear photos is significantly harder for an insurer to dispute.

- Accepting the First Check as a “Final” Settlement: In the rush to get back to normal, many homeowners sign a “Full Release” early in the homeowners insurance claim process. Never sign a document stating the claim is “full and final” until your contractor has finished the work and you are certain there is no hidden damage.

- Assuming Everything is Covered: Many people are surprised to find that while “Wind” is covered, “Flood” or “Sewer Backup” may not be. Reviewing your exclusions before filing can help you frame your claim correctly and manage your expectations.

By remaining aware of these hurdles, you can navigate the property damage insurance claims process with a much higher success rate and ensure that your home is restored to its proper condition.

Frequently Asked Questions (FAQ)

Navigating the aftermath of home damage is stressful, and the homeowners insurance claim process can often feel overwhelming. Below are detailed answers to the most common questions regarding property insurance claims to help you move through the recovery process with confidence.

The timeline for property damage insurance claims can vary significantly based on the complexity of the damage and the volume of claims your insurer is handling. In standard cases, such as a localized pipe burst or small fire, the initial inspection usually occurs within 48 to 72 hours, and a settlement offer may be issued within two weeks. However, following major regional disasters like hurricanes or wildfires, the homeowners insurance claim process can take several months due to the sheer number of affected policyholders and the limited availability of adjusters.

According to the Insurance Information Institute, most states have laws requiring insurance companies to acknowledge a claim within a certain number of days and to accept or deny the claim within a specific timeframe (often 30 to 60 days). To speed up your property insurance claims, ensure you provide all requested documentation immediately and maintain a proactive communication log with your adjuster.

It is not uncommon for a homeowner to receive a settlement offer that is lower than the quotes provided by local contractors. This often happens because the insurance adjuster uses “national average” software for labor and materials, which may not reflect current local construction costs. If you find that your property damage insurance claim payout is insufficient, do not sign a final release. Instead, provide your insurer with the itemized quotes from your independent, licensed contractors.

You can request a “supplemental claim” if “hidden damage” is found once repairs begin. If the insurer still refuses to budge, you may invoke the “Appraisal Clause” in your policy, which allows for an independent third-party to determine the fair value of the loss. Groups like United Policyholders recommend this as a formal way to resolve disputes within the homeowners insurance claim process without immediately resorting to litigation.

One of the most frequent concerns regarding homeowners insurance claims is the impact on future premiums. While a single claim for an “Act of God” (like lightning or wind) may not always lead to a rate hike, your premium is based on a risk assessment. If you file multiple property insurance claims within a three-to-five-year window, the insurance company may view you as a high-risk client.

This history is tracked in a national database known as the C.L.U.E. Report (Comprehensive Loss Underwriting Exchange). According to LexisNexis, insurers use this data to determine your eligibility and rates. In some cases, frequent claims can lead to a “non-renewal” notice, forcing you to seek coverage from more expensive “surplus lines” carriers. It is always wise to compare the repair cost against your deductible before initiating the property damage insurance claims process.

During the homeowners insurance claim process, you may encounter different types of adjusters. A Staff Adjuster or Independent Adjuster is sent by the insurance company; their job is to evaluate the damage and determine what the company is legally obligated to pay according to your policy. Their services are free to you, but their primary loyalty is to the insurer.

A Public Adjuster, however, is a private professional you hire to represent your interests. They handle the documentation, negotiation, and communication for your property insurance claims. While they can often secure a higher settlement, they typically charge a fee, usually between 10% and 15% of the final payout. Hiring a public adjuster is often beneficial for high-value or complex property damage insurance claims where the homeowner feels the insurer’s offer is unfairly low.

Yes, property insurance claims can be denied for several reasons, the most common being that the damage was caused by an “excluded peril.” For example, standard policies typically exclude damage from floods, earthquakes, or general “wear and tear” (maintenance issues). A claim might also be denied if the insurer believes the damage occurred before the policy was active or if the policyholder failed their “duty to mitigate” further loss.

If your claim is denied, the insurer is legally required to provide a written explanation citing the specific policy language they are using. If you disagree, you can file an internal appeal with the company’s claims manager. If that fails, your next step should be to contact your State Department of Insurance to file a formal complaint. They can investigate whether the company followed state regulations during your homeowners insurance claim process.

More Home Insurance Resources

Filing property insurance claims is just one aspect of being a responsible homeowner. To ensure you are fully prepared for every stage of the homeowners insurance claim process, we have curated a selection of resources to help you navigate the complexities of property protection with ease.

Explore our other guides to deepen your understanding:

Home Insurance Glossary

If you encountered unfamiliar terms during your property damage insurance claim, our comprehensive glossary provides plain-English definitions for every technical phrase in your policy.

By staying informed, you can ensure that your property insurance claims are handled efficiently and that your most valuable asset remains protected for years to come.