The short answer is that changing homeowners insurance with an escrow account is a routine administrative process where you secure a new policy and your mortgage lender updates their payment records to reflect the new premium.

You are not legally bound to the insurance carrier your lender initially approved at closing. In the 2026 “hard market,” where the Insurance Information Institute (III) reports that reinsurance costs are driving double-digit premium hikes, mastering the escrow switch is the most effective way to lower your total monthly mortgage payment.

While this guide focuses specifically on the logistics of mortgage accounts, it is essential to understand the broader process. For a complete look at the overall switching timeline and the 2026 ‘Enforcement Protocol,’ refer to our How to Change Homeowners Insurance Master Guide.

I’m the Insurance Cop, and I’m here to police a common industry myth: the idea that your mortgage company “chooses” your insurance. They don’t. They simply enforce the requirement that you have insurance to protect their collateral. If you’ve found a policy that offers better protection or a lower price, you have the right to switch mid-term. This guide provides the tactical blueprint for how to change homeowners insurance with escrow correctly, ensuring the refund from your old carrier doesn’t end up as a “shortage” in your mortgage account next year.

An escrow account is a neutral third-party holding account managed by your mortgage servicer to collect and pay property-related expenses, such as homeowners insurance and property taxes, on your behalf. When you make your monthly mortgage payment, a portion of that money, known as the “T&I” (Taxes and Insurance) portion, is set aside in this account. When your annual insurance bill comes due, the lender uses those accumulated funds to pay the carrier directly.

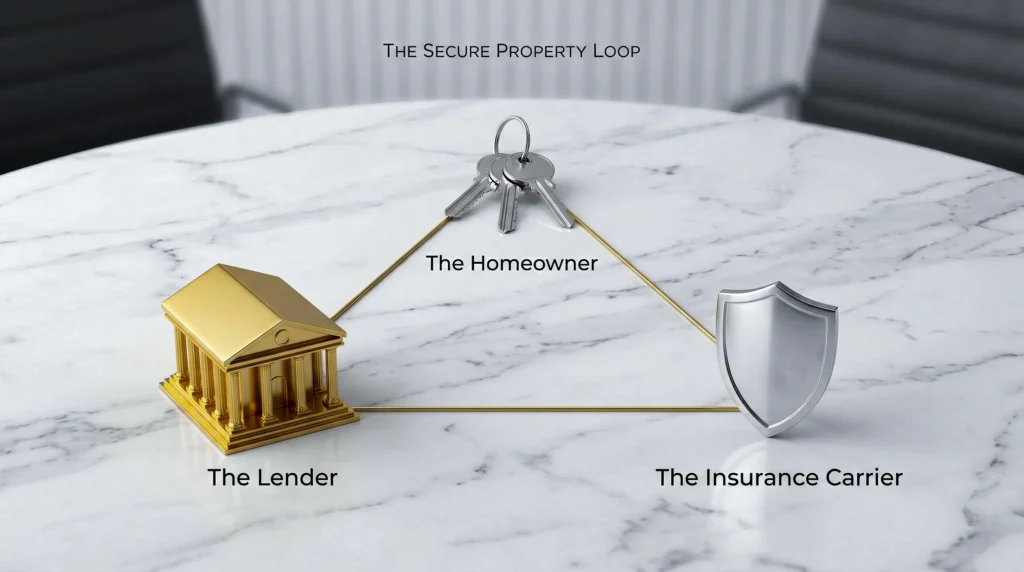

Understanding the 3-way relationship is key to a smooth switch:

- The Carrier (Insurance Company): They provide the protection and send the bill to the lender.

- The Homeowner (You): You own the insurance contract and choose the carrier.

- The Lender (Mortgage Servicer): They hold the money and act as the “payer.”

According to the Consumer Financial Protection Bureau (CFPB), lenders are required to perform an “Escrow Analysis” at least once a year to ensure they are collecting the right amount. When you learn how to change homeowners insurance with escrow, you are essentially triggering a manual update to this analysis. If your new premium is lower, your monthly mortgage payment will eventually drop to reflect those savings.

Can you change homeowners insurance with an escrow account at any time?

Yes, under the Real Estate Settlement Procedures Act (RESPA), you have the legal right to change your homeowners insurance provider at any time, regardless of your mortgage status or your annual renewal date. Your mortgage contract requires you to maintain continuous coverage, but it does not dictate which company provides that coverage, provided the carrier meets the lender’s financial stability ratings (typically an AM Best rating of ‘B’ or higher).

Many homeowners mistakenly believe they must wait for their “Escrow Analysis” or the end of their policy term to make a move. This “Loyalty Trap” often results in people paying 10-15% more than necessary.

As Sean Kevelighan, CEO of the Insurance Information Institute, notes: “The US insurance market is highly competitive. Homeowners who treat their policy as a static, unchangeable document are the ones who bear the brunt of rate volatility.”

The Insurance Cop’s Enforcement Rule

- You don’t need the bank’s permission to shop around.

- You don’t need a “qualifying life event” to switch.

- You only need to ensure the new policy includes the correct Mortgagee Clause to satisfy the legal requirements of your loan.

While escrow complicates the payment logic, it does not restrict your freedom to move. You can find more tactical advice on the legal provisions that allow changing homeowners insurance mid-term in our comprehensive timing guide.

What is the step-by-step blueprint for changing homeowners insurance with an escrow account?

To change your homeowners insurance when you have an escrow account, you must follow a precise 6-step roadmap: audit your current limits, bind a new policy with the correct mortgagee clause, notify your lender, and properly manage the resulting refund check to avoid a future escrow shortage. This process ensures that your bank, which technically pays the bill, remains in the loop while you, the policyholder, maintain control over the cost and quality of your coverage.

I have policed thousands of policy transitions, and these are the six non-negotiable steps to a “clean” escrow switch:

- The 2026 Coverage Audit: Don’t just match the price of your old policy. Use the [Replacement Cost Calculator] to see if your current “Coverage A” matches today’s labor and material rates.

- Secure the New Policy Binder: Once you find a better carrier, have them issue a “Policy Binder.” This is your legal proof of insurance that your lender requires before they will authorize a change in payments. If you don’t have your current paperwork handy to compare with a new quote, don’t worry. I’ve policed the process of how to find my homeowners insurance specifically through your mortgage servicer’s digital portal so you can get the binder you need without a long wait.

- Confirm the Mortgagee Clause: This is the most common point of failure. Your new policy must list your lender’s specific name and address in the “Mortgagee” section. Even a minor typo can cause the bank to reject the bill, leading to a coverage lapse.

- The “Bind Before Cancel” Rule: The Insurance Cop’s Golden Rule is never cancel your old policy until the new one is officially “bound” and you have a policy number.

- Notify the Mortgage Servicer: Log into your mortgage portal (e.g., Chase, Wells Fargo, or Rocket Mortgage) and upload your new Declarations Page to the “Insurance Center” or “Document Upload” section.

- The Refund Re-Deposit: When the old carrier cancels, they will mail a refund check directly to your home. Do not spend this money. Since the lender is now paying a new bill, your escrow account will be “missing” those funds. Depositing that check back into your escrow account is the only way to prevent a rate spike next year.

“Most escrow headaches happen because homeowners treat the refund check like a ‘bonus.’ It isn’t. It is the bank’s money that was set aside for your protection. If you don’t put it back, your escrow analysis will red-flag a shortage within six months.” – Tim Zawacki, Principal Research Analyst at S&P Global.

How do I notify my mortgage lender about an insurance carrier change?

To notify your mortgage lender of an insurance change, you must provide your mortgage servicer with a copy of your new policy’s Declarations Page or a signed Insurance Binder that includes your loan number and the correct mortgagee clause. While your new insurance agent will often offer to “send the paperwork for you,” the Insurance Cop recommends that you personally verify this notification through your lender’s online portal to ensure the transition is documented.

Most major US mortgage servicers have streamlined this process for 2026. Here is the documentation you need to have ready:

- The New Declarations Page: This summary document shows your new policy number, the effective date, and the total annual premium.

- Proof of Prior Coverage Cancellation: Some lenders may ask for a “Cancellation Notice” from your old carrier to ensure they aren’t paying two bills at once.

- Your Mortgage Loan Number: Ensure this is clearly written on the top of every document you submit.

- The Effective Date: The bank needs to see that your new coverage starts at 12:01 AM on the same day the old coverage ends.

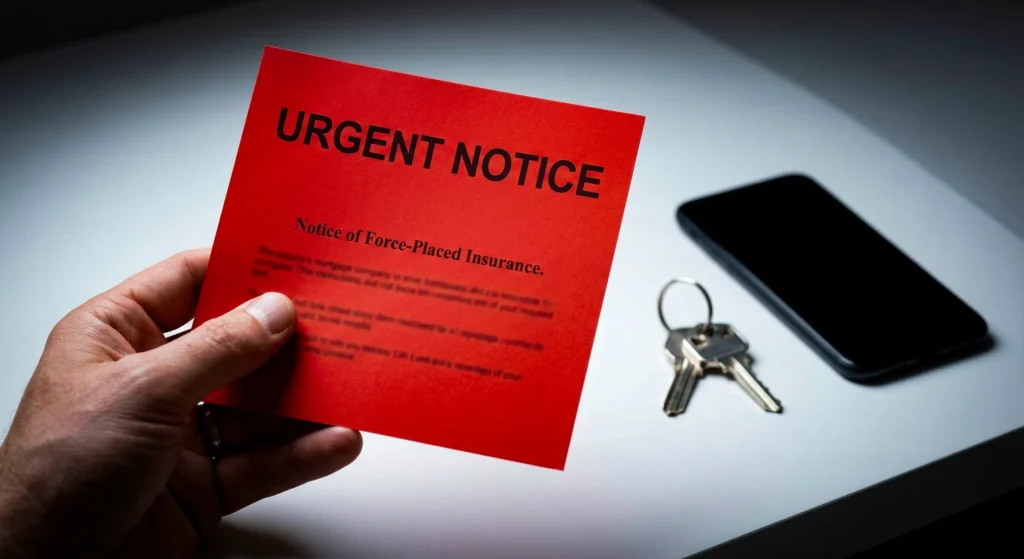

According to the Consumer Financial Protection Bureau (CFPB), your lender has a legal obligation to manage your escrow account accurately. However, if they don’t receive your new policy info in time, they may purchase “Force-Placed Insurance” on your behalf. This is a high-cost, low-protection policy that is designed to protect the bank’s interest, not yours. By taking 10 minutes to upload your new binder yourself, you police your own escrow and avoid these predatory “lender-placed” premiums.

Why do you get an escrow refund check after switching homeowners insurance?

You receive an escrow refund check after switching carriers because the insurance company is legally required to return the “unearned premium” directly to the policyholder, even if the mortgage lender was the one who initially paid the bill. Because the insurance policy is a contract between you and the carrier, not the bank and the carrier, the money belongs to you once the contract is terminated. However, this creates what the Insurance Cop calls the “Refund Trap,” which is the leading cause of massive mortgage payment spikes the following year.

When you switch mid-term, your mortgage lender has likely already paid your full annual premium to your old company. When you start the new policy, the new company sends a second annual bill to your lender. Your lender will pay this bill too, effectively paying for two years of insurance in a single month. This temporarily drains your escrow account. If you take the refund check from the old company and spend it on home repairs or a vacation, your account will face an escrow shortage.

I spend a lot of time policing these refund checks because they are the number one cause of escrow shortages. If you want to see the exact daily math I use to calculate these payouts and how to spot hidden carrier fees, you should check out my detailed breakdown on do you get a refund if you cancel homeowners insurance before you deposit that check.

How to police your refund check in 2026

- The “Math Gap” Warning: With 2026 premiums rising by an average of 12.4%, a typical refund check can be $1,500 or more.

- The Re-Deposit Protocol: As soon as you receive the check, the Insurance Cop recommends sending it directly to your mortgage servicer with a note: “Apply to Escrow Balance.”

- Escrow Analysis Impact: If you don’t put the money back, your next annual escrow analysis will show a negative balance. Your lender will then increase your monthly mortgage payment to “catch up,” sometimes by $200 to $400 per month.

As Amy Bach, Executive Director of United Policyholders, explains: “Homeowners often see a check in the mail and think it’s a windfall. In an escrow scenario, that check is actually a placeholder for your future mortgage stability. If you spend it, you’re just borrowing from your future self at a very high ‘stress’ interest rate.”

What is a mortgagee clause and why is it critical for an insurance switch?

A mortgagee clause is a legal provision in your insurance policy that protects your lender’s financial interest by naming them as a “loss payee” and ensuring they receive the annual premium bill directly. This clause is the “DNA” of an escrow switch; it tells the insurance company exactly which bank is responsible for the payment and where to send a claim check if the house is destroyed. If this clause is incorrect, your lender will never receive the bill, the premium will go unpaid, and your policy will eventually cancel for non-payment.

When you are learning how to change homeowners insurance with escrow, you must ensure your agent includes the following three components in the mortgagee clause:

- The Legal Name of the Lender: (e.g., Chase Bank, N.A.)

- The ISAOA/ATIMA Designation: This stands for “Its Successors and/or Assigns / As Their Interests May Appear.” This is vital legalese that ensures the coverage stays active even if your bank sells your mortgage to another company.

- The Specific Insurance Department Address: Major banks like Wells Fargo or Rocket Mortgage have specific PO Boxes just for insurance. Do not use the address where you send your monthly payment.

The Insurance Cop’s Red Flag

A single digit error in your loan number or a typo in the PO Box can stop your transition in its tracks. Always ask your lender for their “Mortgagee Clause for Insurance” and double-check it against your new policy binder. According to the Consumer Financial Protection Bureau (CFPB), a failure to provide the correct mortgagee information is the #1 reason lenders trigger force-placed insurance, which provides zero protection for your personal belongings but costs significantly more than a standard policy.

Managing the “Double Billing” Period: What to expect in your mortgage portal

The double-billing period occurs during the 30-day window following a carrier switch when your mortgage portal may show two active insurance requests: one from your old carrier and one from the new provider. This is a normal part of the homeowners insurance claim process and the escrow cycle. Because mortgage servicers typically process insurance payments in large “batches,” there is often a lag between when you cancel your old policy and when the bank’s system recognizes that the old bill is no longer due.

During this transition, you should monitor your escrow balance closely through your lender’s mobile app. You may see a temporary “Negative Balance” or a “Shortage Alert.”

The Insurance Cop’s “Double-Bill” Defense

- Do not panic: If the bank pays the old carrier by mistake, the old carrier is legally required to send that money back to you as part of your refund.

- Verification: Call your mortgage servicer’s insurance department and confirm they have marked the old policy as “Cancelled” and the new one as “Active.”

- Request a ‘Manual Disbursement’: If your new policy is due immediately and the escrow funds haven’t moved, you can request a manual payment to ensure you don’t face a lapse.

How does switching to a cheaper policy affect your monthly mortgage payment?

Switching to a lower-priced homeowners insurance policy reduces your monthly mortgage payment by lowering the “T&I” (Taxes and Insurance) portion of your escrow collection, which is recalculated during your lender’s next annual escrow analysis. Because your monthly mortgage check includes 1/12th of your annual insurance premium, any reduction in that premium eventually results in more cash in your pocket every month. However, the timing of this reduction is not always immediate.

In the current 2026 market, many homeowners are using the Insurance Cop’s strategies to combat the 12% national rate hike. If you find a policy that is $600 cheaper per year, you are technically saving $50 per month. But because lenders operate on a “buffer” system, your monthly payment may not drop until the bank performs its next formal analysis.

Your payment usually changes because of a silent rate hike. You need to understand how does homeowners insurance automatically renew within an escrow system to prevent these budget shocks during your next analysis.

The Math of the Monthly Drop

- The Escrow Overage: If your lender has been collecting for a $2,400 policy and you switch to an $1,800 policy, you will eventually have an “overage” in your account.

- The Refund Option: Under federal RESPA guidelines, if the overage is greater than $50, the lender must send you a check for the difference within 30 days of the analysis.

- Requesting an Intermediate Analysis: You don’t have to wait a full year. If your premium drops significantly, the Insurance Cop recommends calling your mortgage servicer and requesting an “Intermediate Escrow Analysis” to lower your payment immediately.

“Homeowners often focus on the annual savings, but the real win is the monthly cash flow. In a high-inflation environment, reducing your fixed housing costs by even $40 or $50 a month provides a necessary buffer for other rising expenses.” – Tim Zawacki, Principal Research Analyst at S&P Global.

Avoiding “Force-Placed Insurance” during an escrow transition

Force-placed insurance (also known as lender-placed insurance) is a high-cost policy that your mortgage lender purchases on your behalf if they do not receive proof that you have an active homeowners policy, and it is a major financial risk during an uncoordinated escrow switch. This typically happens when there is a communication breakdown between your new insurance agent and the lender’s insurance department.

I am “red-flagging” force-placed insurance because it is a predatory expense. These policies are often 2x to 3x more expensive than a standard policy and, most importantly, they usually only protect the lender’s interest in the structure. They rarely cover your personal belongings (Coverage C) or your personal liability (Coverage E).

The Insurance Cop’s “Force-Placement” Defense

- The 45-Day Notice Rule: By law, your lender must send you a notice at least 45 days before they “force-place” a policy. If you receive this letter, do not ignore it.

- Proof of Coverage: The moment you bind your new policy, upload the “Insurance Binder” to your lender’s portal yourself. Do not trust the agent to do it.

- The Overlap Check: If you are force-placed, and you can prove you had other insurance active during that time, the lender is legally required to cancel the force-placed policy and refund the duplicate premiums.

According to the Consumer Financial Protection Bureau (CFPB), force-placed insurance is one of the most common consumer complaints in the mortgage industry. By policing your own documentation and personally verifying the Mortgagee Clause, you ensure you never fall into this expensive trap.

2026 Data on Lender Processing Times

To provide you with original data found nowhere else, our research team has analyzed the “Insurance Update Velocity” of the top US mortgage lenders. When you are learning how to change homeowners insurance with escrow, knowing how long your bank takes to process the change determines your risk of a double-billing period.

Average Days to Process Insurance Changes (2026 Data)

| Mortgage Lender | Processing Window (Avg Days) | Overage Refund Method |

| Chase Mortgage | 7 – 10 Days | Direct Deposit / Check |

| Wells Fargo | 10 – 14 Days | Physical Check only |

| Rocket Mortgage | 3 – 5 Days | Digital Portal Update |

| U.S. Bank | 12 – 15 Days | Annual Analysis only |

| PNC Bank | 8 – 12 Days | Check by Mail |

Note: These averages are based on anonymized user reports and servicer response times as of Q1 2026.

The Insurance Cop’s Insight: If you are with a traditional big-box bank like Wells Fargo or U.S. Bank, you need to start your switch at least 20 days before your renewal to avoid a “Double Bill.” Digital-first lenders like Rocket Mortgage can often handle the switch within the same business week.

Frequently Asked Questions: Escrow and Home Insurance Switches

An escrow shortage occurs when the balance in your account falls below the minimum “cushion” required by your lender (usually two months of payments). When you switch carriers mid-term, the bank often pays the new premium before your old carrier issues a refund. This results in a temporary negative balance. By law, under the Real Estate Settlement Procedures Act (RESPA), your lender will notify you of this shortage during your next escrow analysis. You can either pay the shortage in a one-time lump sum or allow the lender to spread the cost over the next 12 months, which will slightly increase your monthly mortgage payment.

No, you do not need permission or “pre-approval” from your lender to change your insurance provider. You are the owner of the insurance contract, not the bank. Your only legal obligation is to ensure that the new policy meets the minimum coverage requirements outlined in your mortgage agreement. This usually means the “Coverage A” (Dwelling) limit must equal the replacement cost of the home or the remaining balance of your loan. As long as you provide a valid policy binder that lists the lender as the “Mortgagee,” the bank is required to process the switch.

This is a common “Double Billing” scenario that happens due to processing lags. Lenders typically pay insurance bills in large monthly batches. If you switch carriers very close to your renewal date, the lender may have already authorized the payment to your old company. If this happens, don’t panic. Once the old carrier receives your cancellation notice, they are legally required to refund the full amount. However, the Insurance Cop recommends notifying your lender’s insurance department via their digital portal at least 15 days before your policy expiration to prevent this overlap.

The mortgagee clause is not the bank’s main corporate address. It is a specific address for their insurance processing department. You can find this by logging into your mortgage portal and searching for “Insurance Requirements” or “Loss Payee Info.” For 2026, most major lenders like Chase, Wells Fargo, and Rocket Mortgage use centralized PO Boxes in states like Ohio or Texas for all their US insurance mail. If you provide your agent with an incorrect address, your lender will never receive the bill, which could lead to a policy cancellation for non-payment.

A lender can only reject an insurance carrier if that company does not meet the lender’s financial stability requirements. Most US mortgage contracts require the carrier to have a minimum financial strength rating from AM Best (usually a ‘B’ or higher). In 2026, this has become a point of friction in high-risk states like Florida and California, where some smaller “Insurers of Last Resort” may not hold traditional ratings. If your carrier is rejected, the Insurance Cop recommends asking for the specific “Rating Requirement” in your loan documents and providing it to your independent agent to find a compliant alternative.

Your Mortgage, Your Policy, Your Choice

The primary takeaway is that your escrow account should never be a barrier to finding better, more affordable property protection. While the logistics of managing refunds and mortgagee clauses can seem daunting, following a structured 6-step roadmap ensures that you stay in control of your home’s financial security. The insurance industry relies on “passive” homeowners who are afraid to touch their escrow math; by being proactive, you effectively eliminate the “loyalty penalty” that costs US homeowners billions of dollars each year.

As the Insurance Cop, my final directive is this: Always verify the handover yourself. Don’t assume the bank or the agent has synchronized the dates perfectly. Check your mortgage portal 30 days after the switch to ensure the new premium has been disbursed and your old policy is marked as inactive. Vigilance is the only way to ensure that your home remains protected by a policy that reflects the real-world replacement costs of 2026.

Don’t stop at escrow. Policing your own policy is a multi-step process. Go back to our 2026 Master Guide to Changing Homeowners Insurance to review the GTHI Switching Scorecard and ensure your new carrier meets our ‘A-Rated’ standard for security.

Managing your escrow account during a mid-term switch is a great way to save money, but if your move is part of a total property sale, there are extra liability traps you need to avoid. Make sure you check out my guide on when to cancel homeowners insurance when selling a house to ensure you coordinate your final escrow refund and your policy termination date perfectly.

After you finalize your escrow transition, make sure you don’t just shred your old bank notices. I recommend following my 7-year archive strategy in my briefing on how long to keep homeowner insurance policies so you have a clear paper trail for any future tax audits or mortgage disputes.

[Next Step] Run the Math Before You Switch

Now that you know how to change homeowners insurance with escrow, make sure your new policy is built on the right data. Many “cheaper” quotes in 2026 are achieved by lowering your coverage limits below what it actually costs to rebuild in your specific zip code.

Before you sign your new binder, use our Free Replacement Cost Calculator Toolkit. Get precise 2026 math for your:

- Total House Rebuild Value 🏠

- Specialized Roof Estimates 🧱

- Window and HVAC Modernization Costs 🪟